The next two years are expected to see an expansion of refining capacity that is adequate to supply the market, without being excessive. However, the majority of projects that have been announced for completion after 2027 seem quite speculative. This points to reduced investment activity towards the end of the decade. (last updated in March 2025)

Some notes on methodology

The estimates are based on announced projects that are either considered “firm” or “probable”. Firm projects are those for which the company is believed to have made a Final Investment Decision (FID) and, in many cases, the project is known to be under construction. Probable projects are still at the project proposals phase, are undergoing front end design or have not cleared all regulatory hurdles, but are expected to come to fruition. Projects that are considered speculative are not included in the estimate.

The estimates use information that is based on public announcements or other information as found in the public domain.

The aim is to assume that a project is completed when the impact on product supply is fairly aligned to the design intent. Completion dates based on public announcements lead to systematically optimistic assumptions regarding as to when the increase of supply will truly come to exist. Announcements such as “project completion” or “project commissioning” are taken as meaning that the project is mechanically complete and Ready for Start Up (RFSU). However, the project is still months away from reaching its objectives to supply products.

In some cases, projects are split into parts. For example, it has been widely reported that the three trains of the 615kbd Al Zour refineries came on stream in subsequent phases of commissioning or that the Dangote refinery started up in 2024 as an hydroskimmer operating at partial capacity, so its very large FCC will make an impact only in 2025.

One objective of the estimates is to assess the year-on-year increase in supply of light transportation fuels, to make an idea about whether the portfolio of projects is such that it will create upward or downward pressure on margins. Another objective is to estimate the impact on supply of heavy products. For this reason, for each project or refinery closure there is an estimate of the amount of light fuels or heavy products supply capacity that will be added or removed from the market as a result of the project or the closure. The latest generation of projects includes many refineries with high yields of petrochemicals feed in China. Several other refineries have “conventional” petrochemicals integration, i.e. naphtha is used as petrochemicals feed. These refineries make a lower contribution to the supply of light transportation fuels. By contrast, refinery upgrades alter the relative supply of light and heavy products without changing crude distillation capacity.

There are also a few refinery projects that reduce production of fuels. These are projects to add petrochemicals integration without expanding crude distillation capacity.

The global market witnessed large imbalances between 2020 and 2022, because of the impact of the Covid pandemic on global demand, a net loss of refining capacity in 2020 and 2021, and the subsequent rebound of demand in 2022 and 2023. The model starts tracking the impact of projects on supply from 2022. However, in 2022 most of the expansion of supply was from higher utilization of existing refineries.

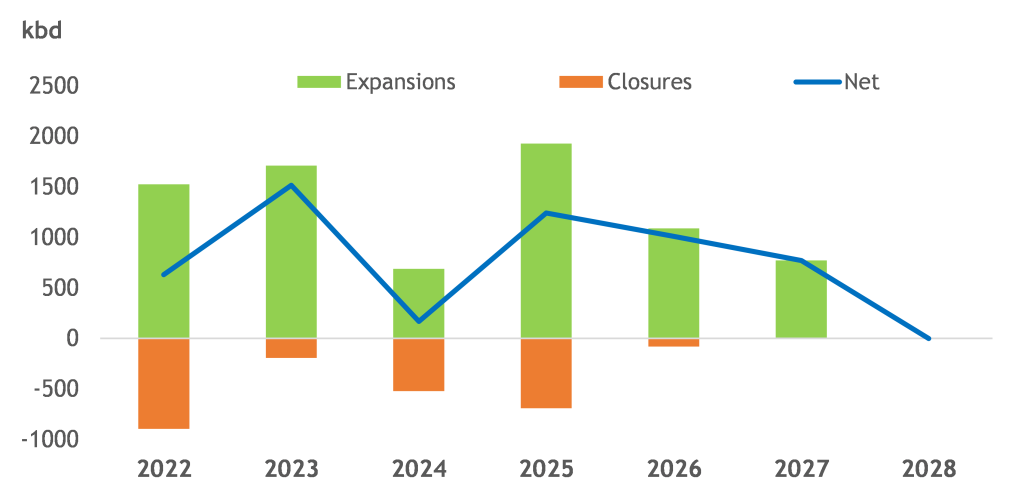

Crude distillation capacity

In 2022 and 2023, about 1.5mn barrels per day of capacity was added, mostly in the Middle East and Asia. However, in 2022 there were also some closures. Most of the closures had been planned with depressed margins in 2020 and 2021 and were executed early in 2022, before margins reached unprecedent levels in the middle of the year. There were also some closures of a cluster of small refineries in China, because the 400kbd Yulong project was implemented by pulling crude oil import rights from some older refineries and giving it to the project. The net result is that the Yulong refinery replaced a group of smaller and older fuels orientated refineries with a new refinery designed for very high yield of petrochemicals.

The most notable developments in 2024 were:

- The partial start up of the Dangote refinery, which reportedly has not reached full capacity and is assumed to have added 300kbd of hydroskimming capacity by Q3 2024. Dangote was mostly notable for the fact its full impact did not materialize and is postponed to 2025

- The bankruptcy of three refineries in China, which removed 400kbd of capacity in the second half of the year

- Completion of the Duqm refinery in Oman

Going forward, there is a good portfolio of projects that are expected to be completed in 2025. However, project development activity seems to have slowed and many projects seems very speculative, with the exception of India and some more petrochemicals projects in China. A project to further expand the Paradip refinery by 200kbd is considered probable, but not expected to be completed before 2029.

There are 689kbd worth of closures that are assumed to happen in 2025. Some are already planned and some have just been announced. A recovery of margins would cause some of these closures to be postponed.

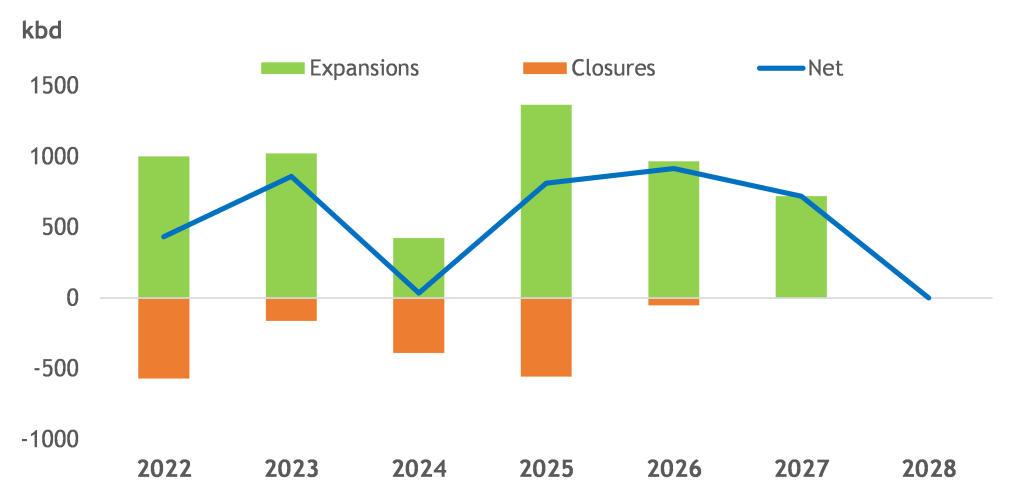

Light products supply

Net expansion of capacity to produce light products has been fairly moderate between 2022 and 2024. This is partly because new capacity was offset by closures and partly because a lot of refineries that were built had very high yields of petrochemicals (in China) or low yields of light fuels (Al Zour).

The year 2025 should see completion of the Dangote project and a good number of other refinery expansions or upgrades being completed. The Yulong refinery had reportedly started crude distillation at partial capacity in mid-2024, but full completion is placed in 2025. Two more petrochemicals orientated refineries should be completed in China in 2025. Although these three refineries have low fuels yields, they should still contribute ~400kbd of light fuels production.

The year 2026 should see the completion of a portfolio of refinery upgrade projects in India. It is also the year in which we have placed final completion of the Olmeca refinery in Mexico.

In the year 2027 we have assumed completion of the Huajin refinery in China, the Chennai refinery in India and completion of some delayed projects to add conversion capacity at Russian refineries.

Refining margins have now settled. Between 2025 and 2027, the expected increase of light product supply arising from projects seems adequate for the consensus forecasts of demand growth, but is not excessive. This points to a supply/demand balance that on a P50 forecast should not change too much, so the direction of margins is not obvious. Refining margins are more likely to be shaped by disruptions or by product demand being unexpectedly high or low.

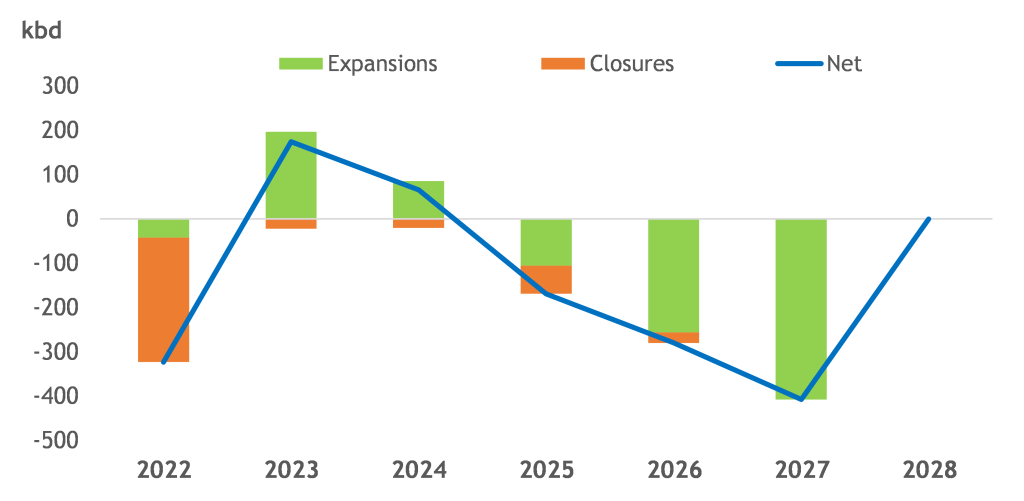

Heavy products supply

Capacity to supply of heavy products is normally removed by refinery projects because new refineries tend to have deep conversion, while some of the existing refineries undertake residue conversion projects or close. The years between 2022 and 2024 were unusual in the fact that quite a lot of new refining capacity did not have full conversion. In 2023 and 2024, fuel oil supply is estimated to have increased, mostly for the contribution of the Al Zour refinery (VLSFO), Beaumont and Dangote. This is not predicted to continue in 2025 and going forward, with the eventual completion of the Dangote FCC, as well as refinery upgrades in South East Asia, India and Russia.

The last 10 years have seen several spells when fuel oil markets were tight and fuel oil prices relatively strong. It seems possible that this will continue to be the case, especially if supply of light crude will continue to grow.

Last revised: March 2025

© Midhurst Downstream, 2025